What This Post Delivers#

You don’t need another indicator. You need a framework that tells you when indicators are worth looking at—and when they’re noise.

Most traders spend years cycling through strategies—moving averages, divergences, order flow, ICT, Elliott Wave—hoping the next method will finally unlock consistent profits. It never does.

Not because the methods lack merit.

Because a method without a framework is just a lottery ticket with a longer expiration date.

This 2,850-word guide dismantles professional trading into its three irreducible components. By the end, you will:

✅ Diagnose exactly why your current approach leaks money—even when you’re “right” about direction

✅ Calculate your true trading edge using the same expectancy formula prop firms use to evaluate traders

✅ Learn why most edges decay—and how to detect yours dying before your capital does

✅ Apply the Partial Kelly Criterion to size positions optimally, not just safely

✅ Walk through a live EUR/USD trade where all three pillars execute in real time

This is not “trading secrets.” This is engineering specifications.

Let’s build.

Introduction: Why 90% of Traders Fail Before They Begin#

The statistics haven’t changed: Of the 10% who are profitable, approximately 90% do not generate returns exceeding passive index investing after accounting for time and cognitive load.

Conventional wisdom blames emotions, discipline, or bad luck. These are symptoms, not causes.

The root cause is structural.

Most traders assemble their practice backwards:

- They start with entries—optimizing, backtesting, obsessing over the perfect signal

- They tack on a stop-loss and call it risk management

- They wonder why they can’t execute consistently

This is like building a house by choosing a front door first.

A professional framework inverts this sequence:

| Priority | Retail Approach | Professional Approach |

|---|---|---|

| 1st | Find winning entries | Define survival: Risk Management |

| 2nd | Add stop-loss | Define edge over time: Probability Thinking |

| 3rd | “Try hard” to be disciplined | Define where edge exists: Market Mastery |

| Last | — | Entries |

If this feels backward, good. That’s the intervention you actually need.

Pillar 1: Market Mastery (How Professional Traders Analyze Market Structure)#

Market Mastery is not pattern memorization.

It is having a causal theory of how and why price moves in the specific instrument you trade. Without causality, you’re not analyzing—you’re guessing with sophisticated tools.

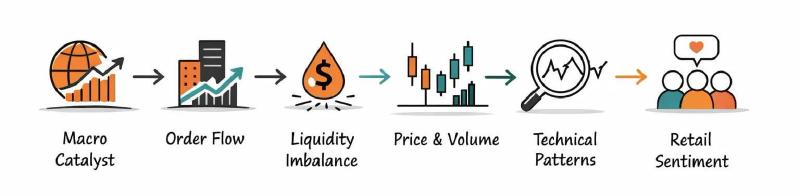

1.1 From Price Print to Price Cause: The Ecosystem View#

The price on your screen is the final output of the following chain reaction. Every price bar is a fossil—the preserved footprint of decisions already made:

[Macro/Fundamental Catalyst] → [Institutional Interpretation & Order Flow] → [Liquidity Imbalance & Market Microstructure] → [Price Movement & Volume] → [Technical Patterns Form] → [Retail Reaction & Sentiment Shift]

Most traders study the last step and ignore everything that preceded it.

They stare at stage five—the footprints—hoping to predict stage six. This is like diagnosing an illness by examining the patient’s shadow. You’ll see distortions. You’ll recognize patterns. But you’ll never understand the cause.

The retail toolbox is built entirely from stage-five instruments. Classical TA, indicators, chart patterns—all describe what price did.

The professional extends upstream—to where price is actually caused. Order flow, microstructure, volume profile—these examine price as it happens.

For a deep dive into the hidden mechanics of institutional order flow—how liquidity, bid-ask spreads, and iceberg orders actually move markets—see our companion guide: Market Microstructure Decoded: How Institutions Really Move Prices.

The table below makes the distinction concrete:

| Approach | What It Studies | When It Forms | Decision Lag |

|---|---|---|---|

| Classical TA | Patterns, support/resistance | After price moves | High (reactive) |

| Indicators | Moving averages, oscillators | After price moves | High (reactive) |

| Chart patterns | Head & shoulders, flags | After price moves | High (reactive) |

| Order flow | Institutional footprint | Stages 2-3 | Low (concurrent) |

| Market microstructure | Liquidity imbalances | Stage 3 | Low (concurrent) |

| Volume profile | Participation levels | Stages 3-4 | Medium |

The synthesis that works:

The goal is not to replace classical technical analysis, but to reposition it in a broader market ecosystem.

Begin with higher-timeframe classical TA (weekly/monthly structure, major support and resistance, macro trend) to define the market’s context—the environment in which price operates.

Then move upstream to stages 1–2 thinking, asking what institutions are likely to do: where liquidity is concentrated, how order flow is structured, what incentives exist for large participants.

In this framework, classical TA becomes a map, not a decision engine. It tells you where the market is, but not why it is there or how it is likely to behave next. The real edge comes from understanding the forces that create price before they are visible on a chart.

This is a shift from pattern recognition to market comprehension—from reading footprints to understanding the terrain that produced them.

For a critical examination of why conventional technical analysis often fails—and what professional traders use instead—read 5 Reasons Why Technical Analysis Fails Most Traders (And What to Use Instead).

1.2 A Pragmatic Map of Market Theories#

If Market Mastery requires synthesis, you first need to know what you are synthesizing.

The problem is not a lack of theories. The problem is that most traders treat these theories as competing religions rather than complementary lenses. They pledge allegiance to one framework and declare all others useless. This is not mastery. This is sectarianism.

A professional does not ask: “Which theory is correct?”

A professional asks: “What does this theory reveal—and what does it obscure?”

Every market theory is a simplification. Each one magnifies certain aspects of price behavior while blurring others.

| Theory Category | Core Premise | Best Application | Blind Spot |

|---|---|---|---|

| Classical TA | Crowd psychology repeats in recognizable patterns | Defining high-probability zones and overall trend bias | Silent on institutional mechanics |

| Order Flow / Microstructure | Price moves reflect institutional liquidity needs | Timing entries/exits; intraday volatility structure | Can overwhelm with noise |

| Wave & Cycle Theories | Markets move in fractal, rhythmic patterns | Identifying potential reversal zones when confirmed | Invites endless reinterpretation |

| Sentiment / Behavioral | Crowd extremes precede reversals | Contrarian signals at statistical extremes | Extremes persist longer than logic suggests |

Read this table not as a ranking, but as a toolkit inventory.

Classical TA gives you the map. Order flow gives you the clock. Wave theories offer a hypothesis about market phase. Sentiment data tells you when the crowd is positioned dangerously.

None are sufficient alone. Each becomes useful when combined with others.

Market Mastery is knowing which lens to apply, when, and how to reconcile their conflicting signals. That reconciliation is not a formula. It is a practiced judgment—and it is the only skill that genuinely separates professionals from amateurs.

1.3 The Mastery Test: Forming a Falsifiable Trading Thesis#

Understanding price structure and market theories is useless if you cannot convert them into a clear trading decision.

Market Mastery is proven at the moment of entry. The question is simple:

Can you translate your market analysis into a falsifiable thesis?

If not, you are trading opinions—not probabilities.

From Opinion to Testable Hypothesis

Most traders think in vague statements:

- “This looks like support.”

- “Buyers should step in.”

- “EUR/USD will probably bounce.”

These are not trade plans. They are predictions without accountability.

A professional trader builds a testable trading hypothesis with three components:

| Component | Purpose | Example |

|---|---|---|

| Thesis | What should happen | Price will hold weekly support and reverse |

| Invalidation | What proves it wrong | Daily close below support |

| Time Condition (Optional) | When it should play out | Within 3–5 sessions |

Without invalidation, you do not have an edge—you have hope.

The Falsifiable Thesis Template

Before every trade, your logic should fit this structure:

“My thesis is that [specific condition will occur]. This thesis is invalidated if [observable price event happens].”

Example:

“My thesis is that BTC will hold prior resistance turned support and produce a higher low. This thesis is invalidated if a 4H candle closes below the zone with expansion volume.”

Notice what is missing:

- No emotional language

- No vague assumptions

- No ego

Just a clear cause–effect relationship tied to observable market behavior.

Why Falsifiability Creates a Trading Edge

A falsifiable trading thesis does three critical things:

- Removes ambiguity – The trade is either valid or invalid.

- Protects psychological capital – You are testing a hypothesis, not defending your identity.

- Builds a data-driven edge – Over time, you learn which conditions truly produce positive expectancy.

This is how professional traders refine strategy performance. They do not ask, “Did I win?” They ask, “Was my thesis valid?”

The Market Mastery Standard

You can evaluate your current level immediately:

- Did I define invalidation before entry?

- Was invalidation objective (price, time, volume)?

- Did I exit immediately when invalidated?

If the answer is no, you are trading intuition—not structured probability. For a complete system to challenge your assumptions before entry, see Why Your Trading Thesis Is Probably Wrong: Beating Confirmation Bias.

Synthesis in Action

This is where Pillar 1 becomes practical. A strong thesis reflects the synthesis discussed earlier:

- Classical TA defines structural context

- Order flow / liquidity explains participation

- Sentiment reveals positioning extremes

- Macro context frames incentives

Example:

“My thesis is that price will find buyers at weekly support aligned with a bullish order block. Retail positioning is heavily short. Invalidation: Daily close below support with expanding volume.”

That is not guessing. That is a causal, testable market hypothesis.

The Core Principle

Market Mastery is not predicting price. It is defining:

- The condition that validates your trade

- The condition that invalidates it

- And exiting immediately when your edge disappears

Over 50 trades, this process builds something far more valuable than a win rate. It builds documented, repeatable trading expectancy. That is the real test of mastery.

Pillar 2: Probability Thinking (Expectancy, Edge Decay & Sample Size)#

Markets are not puzzles to be solved. They are probabilistic environments to be navigated.

This sounds like platitude. Internalizing it rewires how you evaluate every trade—and, more importantly, how you evaluate yourself.

2.1 Your Edge Is Not Your Win Rate: Calculating True Expectancy#

Most traders believe “edge” means “I win more than I lose.” This is incomplete—and dangerous.

Edge is expectancy per unit risk. The formula is simple:

Expectancy = (Win Rate × Average Win) – (Loss Rate × Average Loss)

A trader with a 40% win rate can have a higher edge than a trader with a 60% win rate if their risk:reward ratio is superior.

Example A (Low Win Rate, High Edge):

- Win Rate: 40% | Loss Rate: 60%

- Avg Win: 3.0% | Avg Loss: 1.0%

- Expectancy = (0.4 × 3.0) – (0.6 × 1.0) = 0.6

Example B (High Win Rate, Negative Edge):

- Win Rate: 60% | Loss Rate: 40%

- Avg Win: 0.8% | Avg Loss: 1.2%

- Expectancy = (0.6 × 0.8) – (0.4 × 1.2) = 0.0

Trader B “wins” more often but breaks even. Trader A wins less frequently but has genuine positive expectancy.

The Expectancy Table (Reference):

| Win Rate | Avg Win:R | Expectancy | Verdict |

|---|---|---|---|

| 30% | 4.0:1 | 0.50 | Strong edge |

| 40% | 2.5:1 | 0.40 | Solid edge |

| 50% | 1.5:1 | 0.25 | Modest edge |

| 60% | 1.0:1 | 0.20 | Fragile edge |

| 50% | 1.0:1 | 0.00 | No edge |

Your job is not to maximize win rate. Your job is to maximize expectancy per unit risk.

2.2 Why Your Losses Are Not Errors (And Your Wins May Be)#

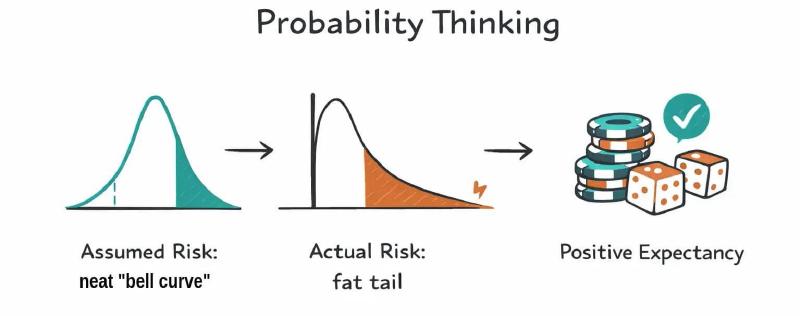

Financial markets do not follow a normal distribution. They exhibit fat tails—extreme events occur far more frequently than standard statistics predict.

This changes everything about how you evaluate yourself:

| Conventional Belief | Probability Truth |

|---|---|

| “A losing trade means I was wrong” | A loss is a required sample in a 45% loss rate |

| “A winning trade means I was right” | A win proves nothing about skill |

| “My last 5 losses mean my system is broken” | 5 losses is statistical noise |

| “I need higher win rate” | You need higher expectancy, not higher win rate |

| “That trade lost because of bad luck” | Luck is always present; edge reveals over time |

If your edge gives you a 55% win rate, you expect to lose 45 out of 100 trades. Those losses are not bugs. They are features of the probability distribution.

The mistake is not the loss. The mistake is:

- The trade taken without edge

- The position sized incorrectly for the distribution

- The failure to take the next valid setup because the last one lost

2.3 Sample Size: How Many Trades Before You Know If You Have Edge?#

This is where most traders self-destruct.

They take 20 trades. They’re down 2%. They conclude: “My edge doesn’t work. Time to find a new strategy.”

You cannot evaluate edge at n=20. You cannot evaluate it at n=50. For most strategies, statistical significance requires 100–200 trades.

Why sample size matters:

| Trades Taken | Observed Win Rate | True Win Rate (55%) | Conclusion Error Risk |

|---|---|---|---|

| 20 | 45% | 55% | 82% chance of false negative |

| 50 | 48% | 55% | 68% chance of false negative |

| 100 | 52% | 55% | 42% chance of false negative |

| 200 | 54% | 55% | 22% chance of false negative |

You do not have a losing system. You have an insufficient sample.

This is not optimism. This is the law of large numbers. Professional traders know that 10–15 consecutive losses can occur within a profitable 55% win-rate system. They expect it. They plan for it.

The 100-Trade Commitment:

Before judging any strategy:

- Execute 100 trades with fixed parameters

- Record expectancy, not just win/loss

- Only then decide: optimize or abandon

2.4 Edge Decay: Why Strategies Die (And How to Detect It)#

Here is the uncomfortable truth most trading courses omit:

Your edge has a half-life.

Strategies decay because:

- Arbitrage closes – Your pattern was exploited; institutions adapted

- Regime shifts – The market environment changed (low vol → high vol)

- Crowding – Too many traders using the same signals

- Your own skill drift – You’re executing differently than when you backtested

The Edge Decay Curve:

Most edges follow this trajectory: Year 1: 0.35 expectancy (discovery) Year 2: 0.28 expectancy (exploitation begins) Year 3: 0.15 expectancy (crowding) Year 4: 0.05 expectancy (decay) Year 5: 0.00 expectancy (death)

How to detect decay before your capital detects it:

- Rolling 50-trade expectancy – If your 50-trade expectancy drops below 50% of its peak, investigate immediately

- Largest losing streak – If you exceed your historical max loss streak by 30%, regime may have shifted

- Fill quality deterioration – Same setup, worse fills; likely crowding

Edge Decay Action Protocol:

| Condition | Action |

|---|---|

| 50-trade expectancy down 30% from peak | Reduce position size by 40% |

| 50-trade expectancy down 50% from peak | Halt trading that strategy |

| Regime shift confirmed (volatility structure change) | Re-optimize parameters on fresh data |

| Crowding suspected (worse fills, same signal) | Move to higher timeframe variant |

You are the casino—but one where the house edge changes slowly over time, and you must continuously verify it still exists.

2.5 You Are the Casino, Not the Gambler#

A casino does not know which roulette number will hit next. It doesn’t need to. It knows that over 10,000 spins, the house edge guarantees profit.

Your edge is your house edge.

It may be small. It may take 100 trades to express itself clearly. But if you have genuine positive expectancy, your job is not to predict—it’s to stay at the table long enough for the math to resolve in your favor.

This reframes everything:

The goal of a single trade is not to make money. The goal is to execute your edge correctly.

Profit is not feedback. A profitable trade taken without discipline reinforces bad habits.

Loss is not failure. A loss taken within plan is successful execution.

The measure of a trade is not whether it won. It is whether you followed your process.

Pillar 3: Risk Management (Position Sizing, Kelly & Capital Preservation)#

Market Mastery identifies opportunity. Probability Thinking frames it correctly.

Risk Management ensures you exist tomorrow to use them.

3.1 The Only Number That Matters: Position Size#

Position sizing is not a risk-management technique. It is risk management itself.

Everything else—stop-loss orders, diversification, hedging—is subordinate to the single question:

“How much of my capital am I exposing to this single event?”

The Percentage Risk Model (Foundation):

Never risk more than a fixed percentage of your current total capital on any single trade.

| Experience Level | Recommended Risk Per Trade |

|---|---|

| New / Learning | 0.25–0.5% |

| Experienced, tested edge | 0.75–1.0% |

| Professional, diversified | 1.25–1.5% (rare) |

| Kelly-optimized | Variable (see 3.3) |

This is a hard constraint. You do not adjust it for “high-conviction” trades. You adjust your conviction to fit your risk parameters.

3.2 From Fixed Fraction to Volatility-Adjusted Sizing#

Fixed percentage risk works. But it ignores market regime.

A 1% risk in low volatility is not equivalent to 1% risk in high volatility. The latter exposes you to greater slippage, wider stops, and fat-tail events.

Volatility-Adjusted Position Sizing:

Position Size = (Account Risk %) / (ATR × 2.5)

Example:

- Account: $50,000 | Risk: 1% = $500

- ATR (14): $1.20 | Stop distance: 2.5 × $1.20 = $3.00

- Position size = $500 / $3.00 = 166 shares/units

Why 2.5 ATR?

Backtesting across multiple asset classes shows 2.2–2.7 ATR captures 75–80% of relevant reversals while avoiding noise. 2.5 is a neutral starting point.

Regime-Based Sizing Table:

| Volatility Regime | ATR Percentile (20d) | Risk Multiplier | Effective Risk |

|---|---|---|---|

| Low | < 20th | 1.2× | 1.2% |

| Normal | 20th–70th | 1.0× | 1.0% |

| High | 70th–90th | 0.6× | 0.6% |

| Extreme | > 90th | 0.3× or sit out | 0.3% |

You do not trade the same size in December (low liquidity, fat tails) as you do in March.

3.3 Optimal Sizing: The Kelly Criterion for Traders#

Fixed percentage risk is safe. It is not optimal.

The Kelly Criterion answers: What percentage of my capital should I risk to maximize long-term growth?

Full Kelly Formula (Simplified for Trading):

Kelly % = Edge / (Average Win / Average Loss)

Where:

- Edge = (Win Rate × Avg Win) – (Loss Rate × Avg Loss)

- Win/Loss Ratio = Avg Win ÷ Avg Loss

Example (Our 40% Win Rate Trader from 2.1):

- Win Rate: 40% | Loss Rate: 60%

- Avg Win: 3.0% | Avg Loss: 1.0%

- Win/Loss Ratio = 3.0

- Edge = 0.6

- Kelly % = 0.6 / 3.0 = 0.20 → 20%

Full Kelly says: Risk 20% of your capital per trade.

THIS IS INSANE.

Full Kelly maximizes growth but creates 30–50% drawdowns. No professional trades Full Kelly. It is mathematically optimal and psychologically impossible.

The Professional Solution: Partial Kelly

Risk Per Trade = Kelly % × 0.15 to 0.25

| Kelly % | 0.15× Kelly | 0.25× Kelly |

|---|---|---|

| 20% | 3.0% | 5.0% |

| 15% | 2.25% | 3.75% |

| 10% | 1.5% | 2.5% |

| 5% | 0.75% | 1.25% |

Most professionals operate at 0.15–0.20× Kelly. This captures 70–80% of optimal growth with 10–15% drawdowns instead of 40%.

Your Position Sizing Framework (Hierarchical):

- Hard cap: Never exceed 1.5% risk per trade (survival constraint)

- Volatility adjustment: Reduce size in high ATR regimes

- Kelly reference: Calculate Kelly; if your fixed % is >0.25× Kelly, reduce size

- Drawdown adjustment: If in drawdown >10%, halve all sizes until recovery

3.4 Rethinking the Stop-Loss: Three Alternatives to “Tight Stops”#

For traders who understand fat tails (Pillar 2) and volatility regimes (Pillar 3), the conventional “tight stop” is often counterproductive. It converts normal market noise into realized losses.

Three professional alternatives:

| Method | Definition | When to Use | Position Size Impact |

|---|---|---|---|

| Thesis-based stop | Level that conclusively invalidates your market thesis | You have clear, testable market structure | Wider stop = smaller size |

| Time-based exit | “If thesis hasn’t manifested within X bars, I exit” | Range-bound markets; low volatility | Same size, fixed duration |

| Volatility-adjusted stop | Stop = Entry ± (2.2–2.7 × ATR) | Highly volatile instruments; earnings | Variable by ATR |

None of these eliminate the need for strict position sizing. They relocate where the risk is taken.

3.5 Portfolio-Level Circuit Breakers#

Individual trade discipline is necessary but insufficient. You must also constrain aggregate risk.

Three non-negotiable portfolio rules:

1. Maximum Drawdown Limit

“If total portfolio value declines 10% from its peak, I cease all trading and reduce to minimum position sizes until I can identify what has changed.”

This is not a pause. It is an investigation. The market regime may have shifted. Your edge may have decayed. You do not “trade through” drawdowns—you diagnose them.

2. Correlation Awareness Holding five tech stocks is not diversification. Holding Bitcoin and Ethereum simultaneously is not diversification.

If your positions share common risk factors, your aggregate exposure is larger than your position-by-position calculations suggest.

Simple test: If news about the S&P 500 or Fed rates would move all your positions in the same direction, you are not diversified.

3. Daily Loss Limit

“If I lose 2× my average daily expectancy in a single session, trading stops for the day.”

This is not emotional. This is circuit breaking. Your cognitive state degrades after unexpected loss. The cost of one revenge trade exceeds the cost of missing one session.

Live Walkthrough: EUR/USD Trade (Three Pillars in Execution)#

Date: February 10, 2026

Instrument: EUR/USD

Timeframe: 4H entry, daily context

Pillar 1: Market Mastery (Thesis Formation)#

Context Analysis:

- Daily structure: Higher highs, higher lows → Bullish trend

- Weekly resistance: 1.1050 (untouched since November)

- Current price: 1.0985, pulling back to previous resistance-turned-support at 1.0950–1.0965

- Order flow: Cumulative Delta showing absorption at pullback—sellers unable to push price through 1.0950

- Sentiment: COT data shows retail net short, commercial net long

Thesis:

“My thesis is that 1.0950–1.0965 will hold as support, attracting buyers for a retest of weekly resistance at 1.1050.”

Invalidation:

“This thesis is invalidated if a 4H candle closes below 1.0940 with expanding volume.”

Time Condition:

“If price has not reached 1.1030 within 5 sessions, thesis is considered invalid.”

Pillar 2: Probability Thinking (Edge Verification)#

Historical Edge Data (Similar Setup, n=78):

- Win Rate: 43%

- Avg Win: 2.8% (of risk)

- Avg Loss: 1.0%

- Expectancy = (0.43 × 2.8) – (0.57 × 1.0) = 0.63

Kelly Calculation:

- Win/Loss Ratio = 2.8

- Edge = 0.63

- Full Kelly = 0.63 / 2.8 = 22.5%

- Partial Kelly (0.18×) = 4.0% → Too high, exceeds hard cap

Decision:

Hard cap (1.0%) is below 0.18× Kelly (4.0%).

→ Use hard cap of 1.0% as binding constraint.

Pillar 3: Risk Management (Execution)#

Account Size: $75,000

Risk Per Trade: 1.0% → $750

Stop Placement: Thesis-based invalidation at 1.0940

Entry: 1.0975

Stop Distance: 35 pips

Position Size Calculation:

- Position Size = Risk Amount ÷ Stop Distance

- $750 ÷ (35 pips × $10 per pip for EUR/USD)

- $750 ÷ $350 = 2.14 mini lots (21,400 units)

Volatility Check:

- ATR(14): 42 pips

- 2.5× ATR = 105 pips

- Actual stop (35 pips) is inside 2.5× ATR → acceptable given clear structural invalidation

Portfolio Status:

- Current drawdown: 3.2% from peak (below 10% circuit breaker)

- No correlated positions open

- Daily loss limit: Not triggered

Outcome:

Price held 1.0952, reversed, reached 1.1038 on session 4.

Trade closed at 1.1030 (55% of target).

Profit: +110 pips × $10 × 2.14 = $2,354 (3.1% account growth)

Post-Trade Review:

- Thesis validated: ✅

- Invalidation respected: ✅

- Position sized correctly: ✅

- Edge calculation accurate: ✅

This is not a “good trade” because it won.

It is a good trade because it was executed exactly as specified by the three-pillar framework.

Conclusion: The Market Rewards Robustness, Not Prediction#

You entered this post searching for an edge.

You are leaving with something more durable: a framework.

The market does not reward intelligence, effort, or even correct predictions.

It rewards robustness—the ability to absorb inevitable shocks, learn from them, and remain operational.

Your three pillars are not aspirations. They are engineering specifications.

| Pillar | Function | Key Metric |

|---|---|---|

| Market Mastery | Your edge hypothesis | Falsifiable thesis |

| Probability Thinking | Your relationship with uncertainty | Expectancy, Kelly, edge decay |

| Risk Management | Your survival constraint | Position size, volatility regime, circuit breakers |

Build them strong. Test them ruthlessly. Return to this page when you feel yourself slipping back into the illusion of certainty.

Then get back to work.

The math doesn’t care about your conviction.

But it does work—if you stay at the table.

📌 Your weakest pillar determines your ceiling.

I read every comment. What’s yours?

This article is part of the Trading Framework Series. For new traders, start with Risk Management First: Why Your Entries Don’t Matter (Yet). For experienced traders, continue to Position Sizing Mastery: The Kelly Criterion and Volatility-Adjusted Sizing.